¿Está su cartera de inversiones preparada para una recesión?

28 de April de 2023

Dónde colocar tu efectivo en tiempos de inflación y recesión

28 de April de 2023

We have heard the word recession so much these days; if you searched for her on Google, you would get more than 239 million results. While it is true that not even economists can agree on whether or not we are in a recession, or if it will arrive if the following is true:

- We are experiencing high inflation, with signs of a slowdown, but it does not seem that it will end as soon as many of us would like.

- People have been getting more into debt.

- The savings of American families has been declining.

- Some companies begin laying off employees.

And to complement, we see that some banks in the United States and the world, as is the case with Credit Suisse and Deutsche Bank, have had their setbacks.

Similarly, according to a CNBC report, there is a 61% probability of having a recession this year 2023, so many may be concerned about their investment portfolio. But with all due respect, if you are fearful for your investment portfolio, perhaps there are certain things that you have not been doing so well and that we could do better.

1.- Recessions are normal processes of the Economies

Many people feel that recessions are rare situations that do not occur with some recurrence, but it is good that we remember that they are natural processes and that nobody likes them. But they appear to correct the imbalances that are generated over time in the economy.

As an article in the Harvard Business Review points out to us, the vast majority of us have lived; the recession from 2007 to 2009, as well as the one produced by the pandemic in 2020. So you can say that you have experienced one of the strongest recessions after the Great Depression; in the same way, it experienced one of the most extreme recessions due to the rapidity of the fall that was the case of the pandemic.

But it has been realized that, in both cases, the capital markets, or the stock market returned to the value it had before the recession began and that rather since then, the markets have risen. At its worst, the Standard & Poor’s 500 reached a value of 676 in 2009, at its lowest point in 2020, it reached 2,237 when writing this article. In April 2023, it was at 4,150 (source: Yahoo Finance).

Now the history of the market

So one of the first lessons, without wanting to make any promise of future returns, is that markets recover over time and that three things can happen:

- You got stressed and sold at the worst moment when you saw that the balance of your portfolio was low, with which there he did kill the possibility of growth, and he was traumatized by what happened to him—never wanting to invest in the capital market again.

- He stayed invested, remembering that this type of situation is normal and that historically the markets recover, and he told himself this money was for the long term. And now I don’t need it, so I better not keep seeing so much news.

- Or the best-case scenario rather invested more when markets fell; because he realized that at that moment, the merchandise became cheaper, and as good merchants do when a good product becomes cheaper, they buy more and save it to sell it at a higher price in the future.

In times of recession, for those who are clear that the capital market is a tool that allows you to reach your long-term destination, it should be seen rather as an opportunity. Because simply in recession, the assets become cheaper; that is what you are looking for to buy more units when the price is lower.

2.- Be careful because you can be the worst enemy of your investment portfolio in times of recession

As technology continues to advance, we have become accustomed to having everything quickly; for example, when I was a kid, if you watched TV, you had to wait for the commercial or advertisement to end to continue watching the show of your choice. Now with Netflix or YouTube, you have So many immediate options that you don’t even have a chance to think about which ones you want to see.

It is there that many people feel that the world of investments should be the same and believe that this is about getting rich quickly, which is fed at the moment with social networks or the stories of someone who became a millionaire by investing in something magical.

But sometimes we forget the words of Sir. John Templeton said:

This implies that although technology has changed and the way to access the market has been democratized, and with any app, you can buy the investment of your choice from your cell phone, there is something that has not changed:

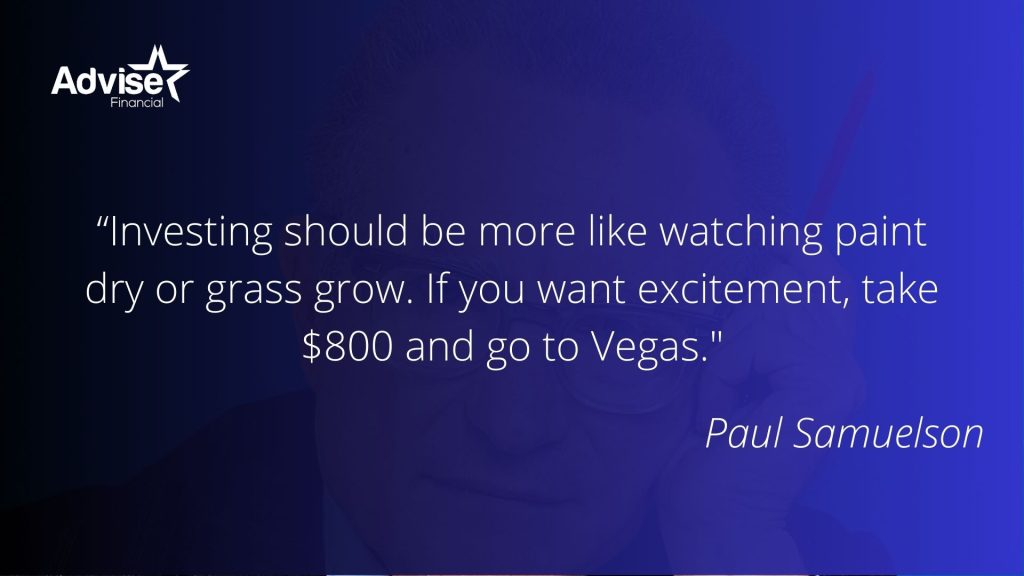

And as Mr. Paul Samuelson said:

All of this that we have discussed sounds extremely logical, but the world of investing isn’t always logical. Because if so, we have already seen it when we saw that the market is going down a lot; you should buy and know that you may have a clearly written Financial Plan to get you to your goals made by a professional like a CERTIFIED FINANCIAL PLANNER™.

But the reality is that we see many investors continue to make the same mistakes when recessions hit.

What happens in recessions?

Because before commenting on these errors, let’s first put in the correct framework that happens in recessions:

According to a report published by Fidelity in 2023, during the last 11 recessions in the United States since 1950, stocks have historically fallen an average of 15% per year and have an average duration of 9 months, with which we could already say that in the case of the fall that the market had during 2022, we would already be above both averages, both by percentage and by time.

Investor mistakes

Main mistakes of investors in times of economic turbulence:

- Your portfolio is not diversified, and you keep betting on a group of individual or particular stocks because you feel that you have the ability to determine as if you were a wizard, which is the winning stock. We have already seen how actions that looked very solid, such as Tesla and Meta, fell sharply in 2022, and although many have recovered, they sold without waiting.

- You panic and continually check your investment portfolio whenever you hear negative news. You think you have the magical power to read the future, but in reality, you sell at the worst time and buy when the markets are already up.

- Beware of magical financial products that offer you high returns and no costs, such as the proliferation that is currently taking place with Structured Notes, which offers precisely this. Remember that in Finance; there is no free lunch; someone always pays the bill and even more so when they don’t know how expensive it can be.

- In times of turbulence, it is not the most appropriate thing to try to manage all your family’s money by relying solely on your instincts, and that is where you should rely on a financial adviser who has more flight hours than you. But above all, always seek your financial well-being by putting your interest above his and be one of those who call Fee-Only so that you do not pay unnecessary commissions and optimize your investments. A good place to look for this type of Advisor is at the NATIONAL ASSOCIATION OF PERSONAL FINANCIAL ADVISORS.

3.- Is this a good time to invest?

The first question you should ask yourself is, do you have the financial capacity to invest right now, and the answer is very simple:

- If you owe money on the credit card now, the rates are at their all-time high.

- You do not have an emergency or savings fund covering several months of your monthly spending.

- You believe that the stock market or some crypto assets will help you to be rich in the short term, and you will invest the money you need in the short term (Less than 3 years).

Of course, you should not invest; rather, it is time to continue strengthening your finances to invest.

If you rather have managed to cover all these previous points and have idle money in your bank account from a large bank earning an interest rate that does not even reach 0.50% per year while inflation is eating that money and you should seek professional help to invest that money.

The next question is how to invest in times of recession.

Some people tell us with these rising interest rates; we should only have Bonds and banking instruments such as Certificates of Deposit and Money Market funds, right?

And although it is true that in times of recession, what happens is that when rates rise, these instruments give good income, and as we saw previously, the shares tend to fall. It is no less true that, as we have said, you would also like to benefit precisely in the long term from the rise in the value of the shares.

So our suggestion remains the same: having a little of everything is important to enjoy all these benefits. That is why you must have a diversified portfolio with stocks and bonds, this being one of the best protection mechanisms, being able to use index funds or ETFs for them.

Dollar Cost Methodology

Additionally, as we have said, it does not try to predict the perfect moment; it uses the methodology called Dollar Cost Average to go buying continuously over time, with which in those moments that the market falls with the same amount, you will buy more units because they are cheaper. If the market goes up, you will buy less because they are more expensive.

Finally, remember that every year Uncle Sam allows you to save and invest in accounts with tax benefits in the United States, such as 401Ks, and IRAs. If you don’t take advantage of and maximize the amount you can contribute, you lose that quota for the year. Not being a very good business that you lose the possibility of legally saving taxes.

In conclusion, we see that the recession for the investment world is bad if you are not ready to invest, do not have a diversified portfolio, or cannot control your fears.

Note: No comments in this article should be taken as investment advice or advice. Always check with your financial advisor before making a decision—information for educational and informational purposes only.

Founder & CEO Advise Financial

Alonso is a “CERTIFIED FINANCIAL PLANNER™” who is dedicated to increasing the Financial Well-being of nurses, physicians and successful immigrants in Florida and Texas. With more than 20 years of experience in the world of finance, always working for the best interest of his clients, under fiduciary criteria.

{kind=link}

{kind=link}

{kind=link}